Getting to $1m in super is within reach (if you start saving early)

Created On: 23/02/2022

One million dollars in your superannuation fund. The task seems daunting, but the dirty little secret is it's an achievable goal. You don't need a massive salary or savings rate to get there. You need the magic of compound interest.

Financial literacy in this country is poor, particularly for women and young people. This translates into a lower quality of life in retirement. Today I'm going to show you what it takes to reach $1 million in retirement using a simple retirement calculator. If you take one thing away from this exercise it should be that saving early in life, and taking advantage of compounding returns, is incredibly impactful later in life. The longer you put off saving, the harder is it to make the time back. That's because money makes money. And the money that money makes, makes money.

If you're a little bit older, or have some gaps in your savings, don't be disheartened. Saving and investing early is the easiest way to reach $1 million, but it's not the only way. Those in their 30s and 40s can still get there, but it takes a lot more sacrifice. What's important is that everyone understands how to make their money work for them and how they're tracking against their goal. Hopefully, this also convinces some to keep their money in super (when given the option to withdraw it early), and not to play around with by taking risky bets. Let's get into it.

Retire a millionaire

Let's say I make a pre-tax salary of $60,000 at age 25. I want to retire by age 67 with $1 million, which leaves me 42 years to reach my goal. How can I get there?

First, 10% of my salary goes into a superannuation fund every year to retirement—the mandatory minimum for employed Australians. Any returns I make are automatically reinvested. I also commit to making voluntary contributions of 2.5%. This can be a hard pill to swallow, especially for young people pushing all their after-tax savings into a mortgage (which will form an essential pillar of retirement). But the tax shield superannuation offers (15%) makes it worth it.

Now I need to make some assumptions:

• I assume the fund returns 7% annually (from the second year). Morningstar data shows AustralianSuper balanced has returned 9.68% annualised since inception but we're going to play it safe. These returns drop to 5% from age 55 to account for a reduction in risk. • I also assume my salary increases 2.5% annually to retirement

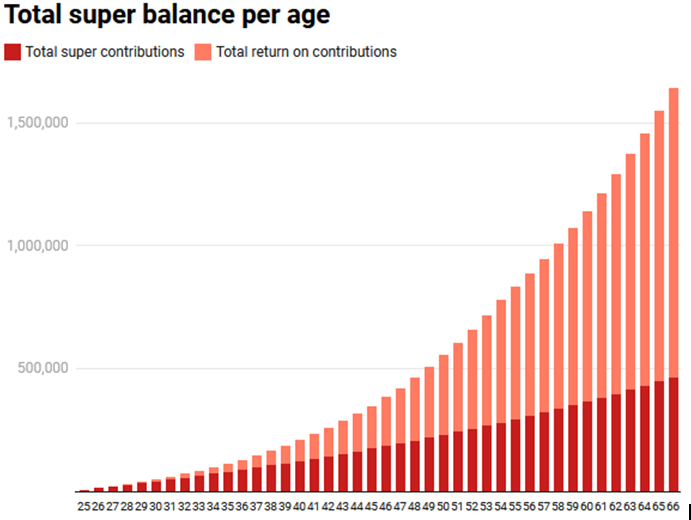

It's said the first million is the hardest and boy is that true. It will take 25 years of diligent saving and investing to reach $500,000 but only another nine years to reach $1,000,000. That's because my retirement savings generate their own earnings, which are reinvested. I will receive interest on the amount I invest from my salary each year, but also on the savings I've built up. By age 66, I have retirement savings of $1,644,221 – which include total savings (after tax) of $464,353 and a total return on investment of $1,179,867. As expected, return on investment starts slow, but comes home strong:

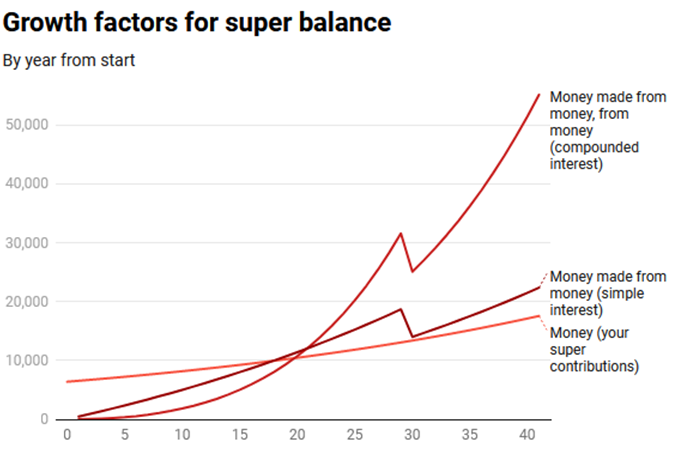

If we break down the yearly flows, you can see from our friend Benjamin Franklin, that our money makes some money, but it's really the money made from our money that's making the money:

Takeaways and caveats

Kids are costly. What struck me doing these calculations is just how important it is to save early in my career. I did a little experiment and calculated the impact of taking 5-years off in my early 30s to have children. My final retirement balanced dropped by $414,424. However, if I'd taken 5-years off work at age 50, the change to my final balance was negligible, only falling by $155,905. As Mark Lamonica said in his webinar last Thursday, young people have time on their side to save and compound returns. If you're going to take time off, consider how it will impact returns, and if you can contribute more once you return to the workforce.

Fees bite.investing isn't free. Investment managers charge fees to invest our money. Assuming annual fees of 1%, my total costs accumulated to roughly $223,700 by retirement. Had I been charged 0.7%, I’d pay $156,600 – a difference of ~$84,000. This highlights just how important it is to be in a low-cost fund. On a one-year basis, fees look negligible, but your lifetime value to a fund is enormous. The effort to retain you should be commensurate, but this isn't always the case. Shop around, make them earn your loyalty.

Don't forget about inflationMoney today isn't worth the same as money 40 years from now. We must account for the impact of inflation (the increase in the price of goods and services) on our dollars.

If we input a long-term inflation rate of 2% into our calculator, the lower end of the RBA's target band, and annual fees of 1%, my $1,644,221 in 2057 means $713,608 in today’s money.

Now, some caveats. My calculator makes a lot of assumptions – namely that your wage will increase 2.5% annually for your entire career. Wages increases don't work like this. Like returns, my assumptions are annualised. Salaries tend to follow a more jagged pattern, with bigger raises some years and stagnation in others.

It also assumes you're with a top performing superannuation fund. APRA data released last week showed up to 1 million Australians are in MySuper funds 'underperforming' the government’s benchmarks. This also highlights the importance of getting good returns out of super.

Remember, superannuation is just one part of our total savings. Assets for funding retirement include any savings/investment we may have outside super including shares and property. Increasing your saving at least 20 per cent of your income is a good goal, particularly when you're young and have the least amount of expenses.

But do I need $1m?

With my 'millionaire' status insight, it's important to ask: Do I really need $1 million in super to retire? No. One million is an ideal – a figure thrown around by financial professionals as an aspiration. Everyone's 'perfect' retirement will depend on the lifestyle they want to lead – when you want to retire, where you live, whether you own your own home, and how many cruises you want to take to Europe. What's important is that you have a figure in mind for your retirement goal and keep track of whether you're on track to meet that goal.

Saving regularly from an early age also gives you optionality. Earlier in life, if something goes wrong or you change your mind about your lifestyle, you can act on that. Later in life, you have fewer options to work or re-educate yourself.

Australia also has an exceptional social safety net in retirement, paying a full annual pension of $37,000 (for eligible couples - combined).

If you'd like some help, there are some useful rules of thumb/guidelines:

• The ASFA retirement standard is an estimate of how much you'll need for a 'modest' or a 'comfortable' retirement (for singles and couples) annually. For those aged 65 today, ASFA suggests a couple need $63,000 annually to live comfortably (if they own their own home).

• Fidelity’s benchmarks are salary-based rules of thumb for retirement savings. 1 x your salary at 30, etc. These guidelines can be appealing because of their simplicity but also daunting for investors who may find themselves running far behind.

If you're reading this in your 30s or 40s and thinking s**t, I'm never going to get anywhere near my goal, use this moment to take control of your retirement. Consider what it would take for you to reach $1 million and what lifestyle changes you'd need to make. The benefit is you probably have a higher salary than a 25-year old and a greater capacity to contribute to your retirement fund. Just remember the tax rates do increase once you contribute more than $27,500 annually.

Retirement calculators and benchmarks are a reasonable starting point. Their greatest value lies in showing that while reaching $1 million is daunting, it's achievable for those who start early and stick with it. Keep track of how you're doing. It doesn't have to be everyday (put away the highlighters) but sit down once a year and ask: am I on track to reach my retirement goals? If not, consider setting aside more the following year.