RETIREES: HOW TO BEAT INFLATION BEFORE IT BEATS YOU

Created On: 09/03/2022

Investors with long memories – or a good education – will recall the bad old days when inflation was the economic bogeyman. It broke Germany’s Weimar Republic in the 1930s and nearly cratered America’s economy in the 1970s

Fortunately, inflation has been a non-issue in Western economies for decades. But is that about to change? In the first quarter of FY2021, Australian inflation ran at a comfortable 1.1%. By the second quarter it had leaped to 3.8%.

Perpetual Private’s June Quarterly Update summed up the problem: “With very easy monetary policy likely to continue for the next couple of years, and government spending at record-breaking levels, there remains the risk that inflation could become out-of-control. Historically, high levels of inflation have been very difficult to contain once in place."

INFLATION HURTS RETIREES

Inflation is bad news for retirees. "A continual rise in the price of goods and services can really affect someone who's retired or approaching retirement", says Malissa Tobias, a Perpetual Private adviser in Melbourne. "Inflation eats your purchasing power - you get fewer goods and services for the same amount of money."If you're still working your salary can rise to keep pace with inflation. Retirees - especially those with money in low-rate assets like term deposits or cash - suffer because their spending power is cut and the real (after-inflation) value of their capital is falling.

"Inflation is when you pay fifteen dollars for the ten-dollar haircut you used to get for five dollars when you had hair." Sam Ewing[1]

QUANTIFYING THE PROBLEM

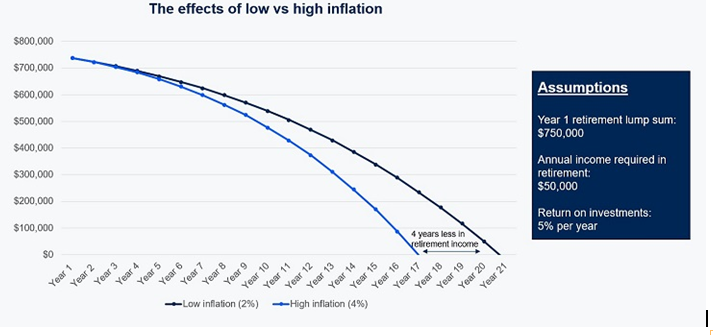

Because inflation erodes the value of your money it reduces the life span of your super savings. To illustrate this, the graph below shows the effects if inflation runs at 4% rather than 2%, you'll run out of money at year 17 - four years earlier. To put that 'high' 4% number into deeper context, Australian inflation averaged over 8% in the 1980s.[2]

Source: Perpetual

Past performance is not indicative of future performance

According to Malissa Tobias, retirees and near-retirees have four core anti-inflation strategies.

ONE: MANAGE YOUR RETIREMENT

By managing the timing and shape of your retirement you can offset some of the inflation threat.If you work a little longer (either full or part-time) you can earn an income that might go up with inflation. Those extra earning years also give you more time and money to build up the largest possible nest egg to generate your retirement income. Finally, but just as importantly, retiring later delays the day you start drawing on your capital.

"There will always be people who need to retire on a given date", says Malissa Tobias. "They might have health problems or just reached the point where work is no longer rewarding. But for many others, delaying retirement keeps them tied to people or activities that bring them joy. If it boosts their retirement savings and extends the life of their nest egg, so much the better."

TWO: INVEST IN INFLATION-BEATING ASSETS

Investing in higher-returning assets - like shares or property - can deliver the same benefits as earning work-income because their value can rise in line with, or above, the rate of inflation.The inevitable complication is that higher returning assets are usually higher risk assets. "To take into account inflation, we would need to consider investing in growth assets for a retiree’s portfolio", says Malissa Tobias. "So, I work through the issues to make sure they're comfortable with a more aggressive approach."

Perpetual Private actively manage that extra risk by:

• Investing in high-quality growth assets.

• Diversifying investments so that falls in one security or asset class don't have outsize impact. A wide spread of assets also gives retirees more sources of return.

• Tailoring the growth strategy to the client's needs. This ensures the strategy and level of risk aligns with the client’s risk tolerance.

THREE: PLAN YOUR SPENDING

"Knowing how much money you're going to need in retirement is a crucial part of our planning", says Malissa. "We do sophisticated modelling to budget for a client's income needs and account for tax and inflation. The modelling helps us deliver the income they need and minimises how tax and inflation affect their retirement lifestyle."FOUR: DRAW ON CAPITAL

The recent Retirement Income Review suggested many retirees die with their capital intact. But that's not the case for everyone. In a world where the threat of inflation is rising, some retirees will need to dip into their capital to fund the retirement lifestyle they want. The key is to do that prudently."The idea that you should live only off the income from your retirement portfolio is a bit of a myth especially if it crimps your lifestyle", says Malissa. "The aim, always, is to craft realistic spending and investment strategies that beat inflation and take into account clients income needs and how long they need their money to last."

MALISSA'S REAL-LIFE CASE STUDY: STAY ON TARGET

"After selling his home, one of my clients retired with $2 million to invest in 2009. He had an ambitious income target - he wanted to enjoy life and needed $180k a year to do it.We did the numbers together and it was clear he’d need a high allocation to growth assets such as property and Australian and International shares to reach that goal. Despite the extra risk that involved – and the fact that we were in the midst of the GFC when many investors were feeling nervous – he committed to the strategy and stayed the course through the markets’ ups and downs.

We recently did the numbers on the strategy and the client’s portfolio balance has been maintained at $2m despite the client withdrawing on average $226,000 per annum of retirement income over the 12 year period.

The most important thing my client had going for him was the clarity of his approach. He knew what he wanted and we worked together to get him there.

The lesson is not that every retiree needs an aggressive asset allocation to generate the income they need and beat inflation. It’s that being clear about your goals means you can make intelligent risk/return trade-offs that give you the best chance of getting the lifestyle you want."